What You Must Know About AVCS Pension in the UK?

Many people in the UK worry if they will have enough money when they stop working. A workplace pension may not always be enough. This is why some people use an AVCS pension. AVCS stands for Additional Voluntary Contributions. It is a way to add extra money to your pension savings.

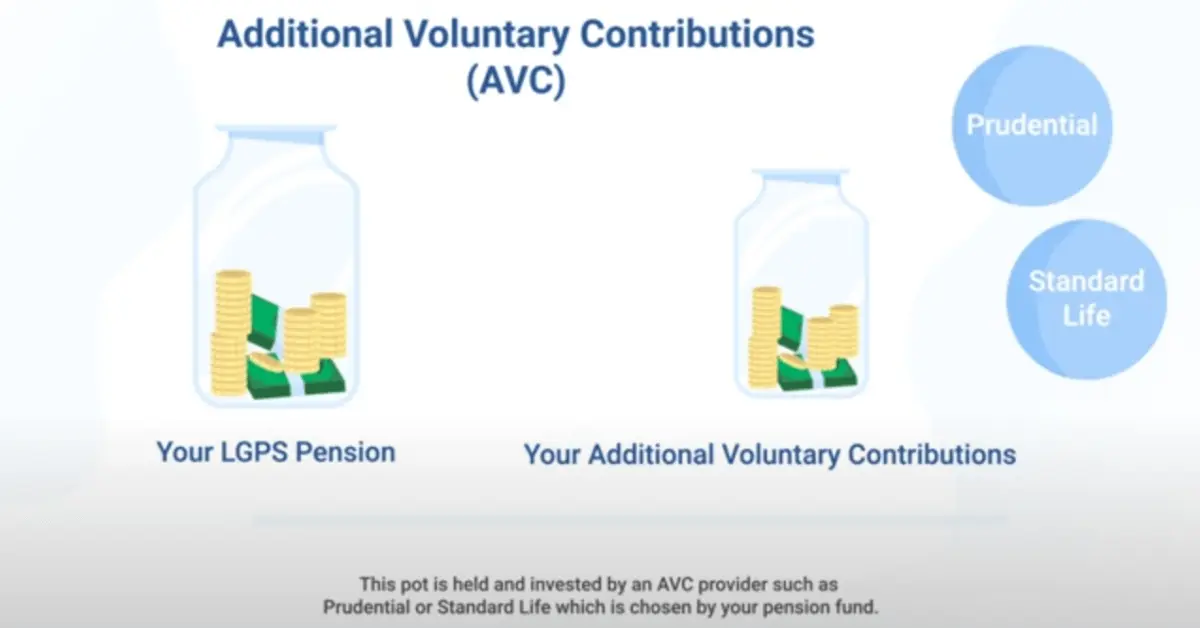

What Is an AVCS Pension?

An AVCS pension is extra money you choose to pay into your workplace pension. You decide how much to put in. This money is then invested to help it grow. Many workplaces use a provider like Prudential to manage these extra payments. The good thing is that you can change how much you pay if your money situation changes. You can stop, start, or change the amount when needed.

How Tax Relief Helps You?

One of the biggest reasons people like an AVCS pension is tax relief. This means the government gives you back some of the tax you pay when you put money into your pension.

Also Read: What to Look for When Choosing Insurance?

For example, if you put in £80, the government adds £20. So, £100 goes into your pension, but it only costs you £80. If you pay a higher rate of tax, you can get even more back. This makes saving easier because you get more for your money. But you must stay under the yearly pension limit. If you go over, you may have to pay extra tax.

What Teachers and NHS Staff Need to Know?

If you are a teacher or NHS worker, you have special AVC options. The Teachers Pension Scheme and NHS Pension Scheme both let you add extra money.

These schemes can also help you pay less tax and National Insurance. Many public workers use this to grow their pension without losing too much from their pay each month. Even small amounts can grow over time. For example, putting away £50 a month may not feel like much now, but after many years it can turn into a big sum.

Picking the Right Provider and Plan

Many public workers have their AVC managed by Prudential. They offer different investment plans. Some are for people who want to take more risk to grow their money faster. Others are safer but grow slower.

You should think about your own situation. A young worker might take more risk because they have time to recover from losses. An older worker might want to keep their savings safe. It is a good idea to check the fees for each plan. High fees can reduce how much you save in the long run.

A Simple Example to Understand

Let’s take Tom, a 35-year-old NHS worker. He decides to pay £150 a month into his AVC pension. With tax relief, it only costs him around £120.

If Tom keeps doing this until he is 65, and his money grows over time, he could have a pot worth over £90,000. This is on top of his main NHS pension. This extra money can help him enjoy a better life when he retires.

What to Watch Out For?

There are some things you should keep an eye on. Make sure you do not go over the yearly limit for pension payments. If you are close to it, talk to someone or check with your pension provider.

Also, remember that investments can go up and down. You might get back less than you put in if the market does badly. When you retire, you can usually take a part of your pension as a tax-free lump sum. Think about whether you want to take some money at once or leave it to give you an income over time.

Final Thoughts

An AVCS pension is a simple way to save more for your future. With the help of tax relief, your money can go further. Whether you are a teacher, an NHS worker, or another UK employee, adding a bit extra now can help you enjoy life more later.

Take the time to look at your choices. Check how much you can afford. Review your plan every few years. And if you are unsure, get advice. A small step today can make a big difference for your tomorrow.